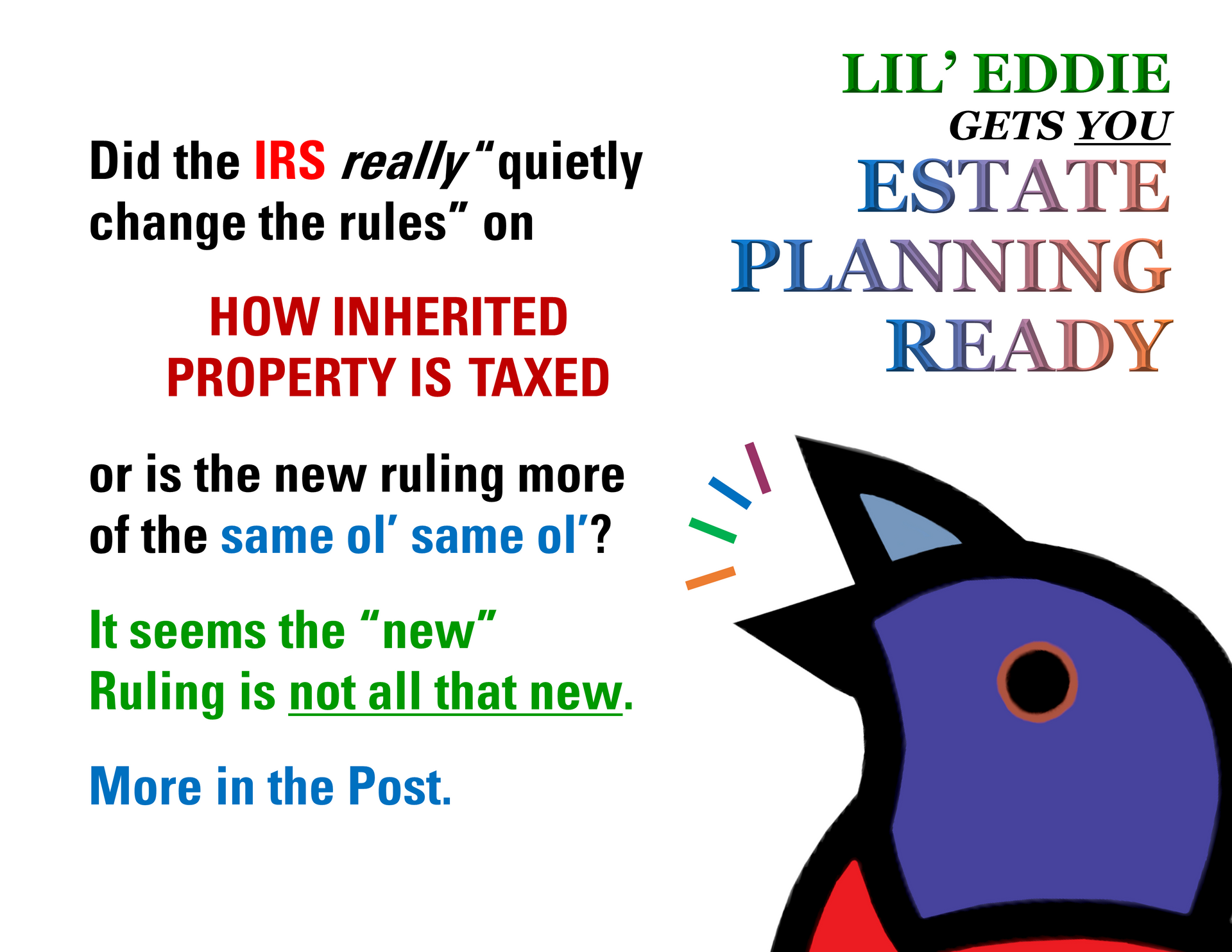

Did the IRS REALLY "quietly change the rules" on how inherited property is taxed?

Revenue Ruling 2023-2 is old news.

Some of you may have come across a recent tax article with a bone-chilling headline:

IRS Quietly Changed the Rules on Your Children’s Inheritance.

Fear not, my friends! Let me clarify the situation for you. The truth is that Revenue Ruling 2023-2, which has been making headlines, merely formalized what tax and trust attorneys have been aware of and practicing for years. If you have been working with anyone but the most aggressive tax professionals, there is likely no recent rule change that endanger your child’s precious inheritance, quiet or otherwise.

In a nutshell, Revenue Ruling 2023-2 states that assets which are not part of your estate when you die will not receive the coveted

step-up in basis, wherein an inherited property's "purchase price" (basis) is stepped-up to the fair market value of the asset at the owner's death. Hardly a new change, this concept has been a fundamental principle of tax planning since time immemorial, harkening back to the days when early humans pondered the complexities of tax and asked themselves, "Should I give my cave to my children now, thereby excluding it from my estate for estate tax purposes (in increments below the annual gift tax exclusion of course), or should I consider its step-up in basis for capital gains tax purposes so my children receive less of a tax hit when they realize the gain?"

What’s the key takeaway here? You need to decide whether to prioritize

(1)

capital gains tax planning

or

(2)

estate tax planning. For 2023, estate taxes only come into play if your estate exceeds $12.92 million, so most people will focus on capital gains tax benefits. But remember, individual circumstances vary, and it's crucial to engage in this kind of planning under the guidance of a knowledgeable trust and tax attorney.